It’s November 19 and we are in a weird place with food inflation.

Everyone has already seen the “3% food inflation” charts from late summer. At the same time, the government hasn’t released October inflation data and there is a real chance that gap in the official data never gets fully filled in. So the number that is supposed to describe reality today is still data from September.

Grocery prices are still super high.

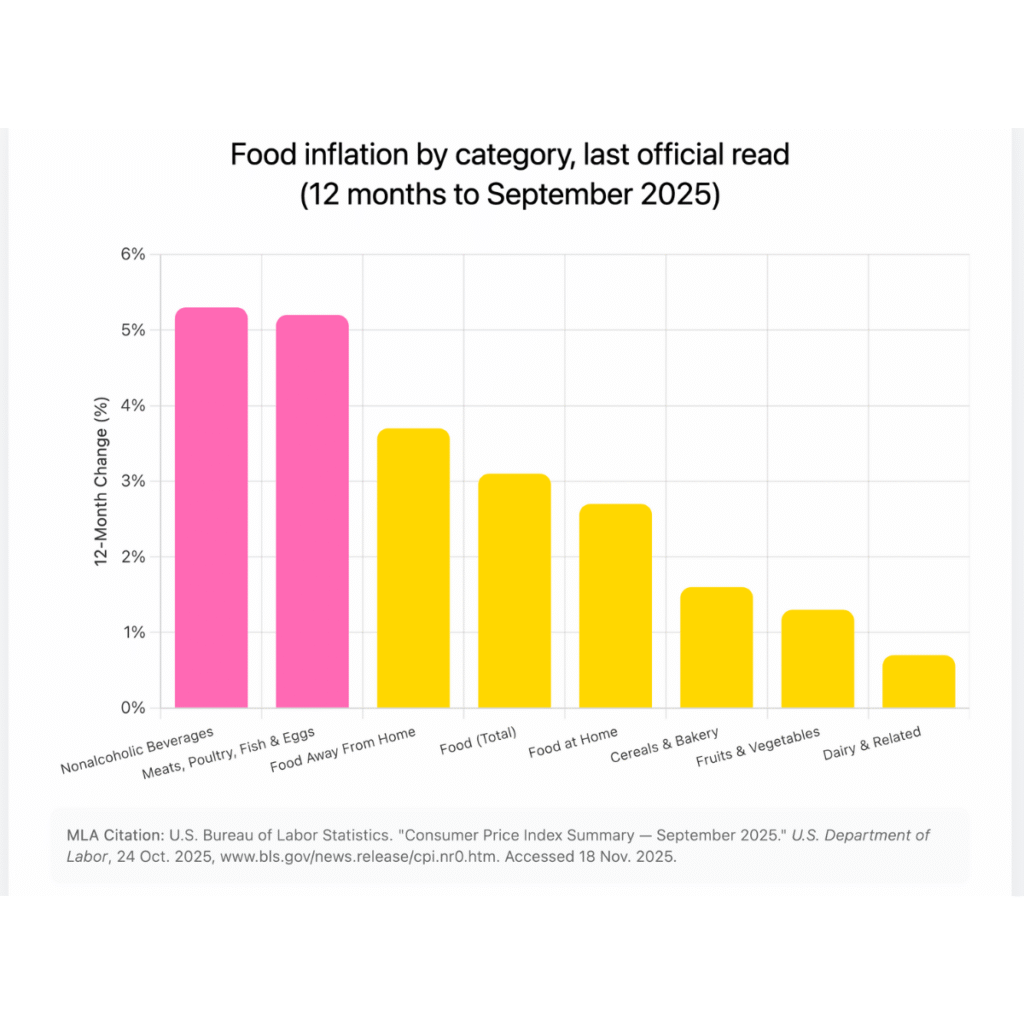

The last detailed read we have from the Bureau of Labor Statistics showed food up just over 3% and food at home a little bit under that. While that’s useful as a starting line, it’s not extremely helpful as an answer for what is happening in mid November.

Since September, we moved into the most important grocery season of the year and the market is heating up.

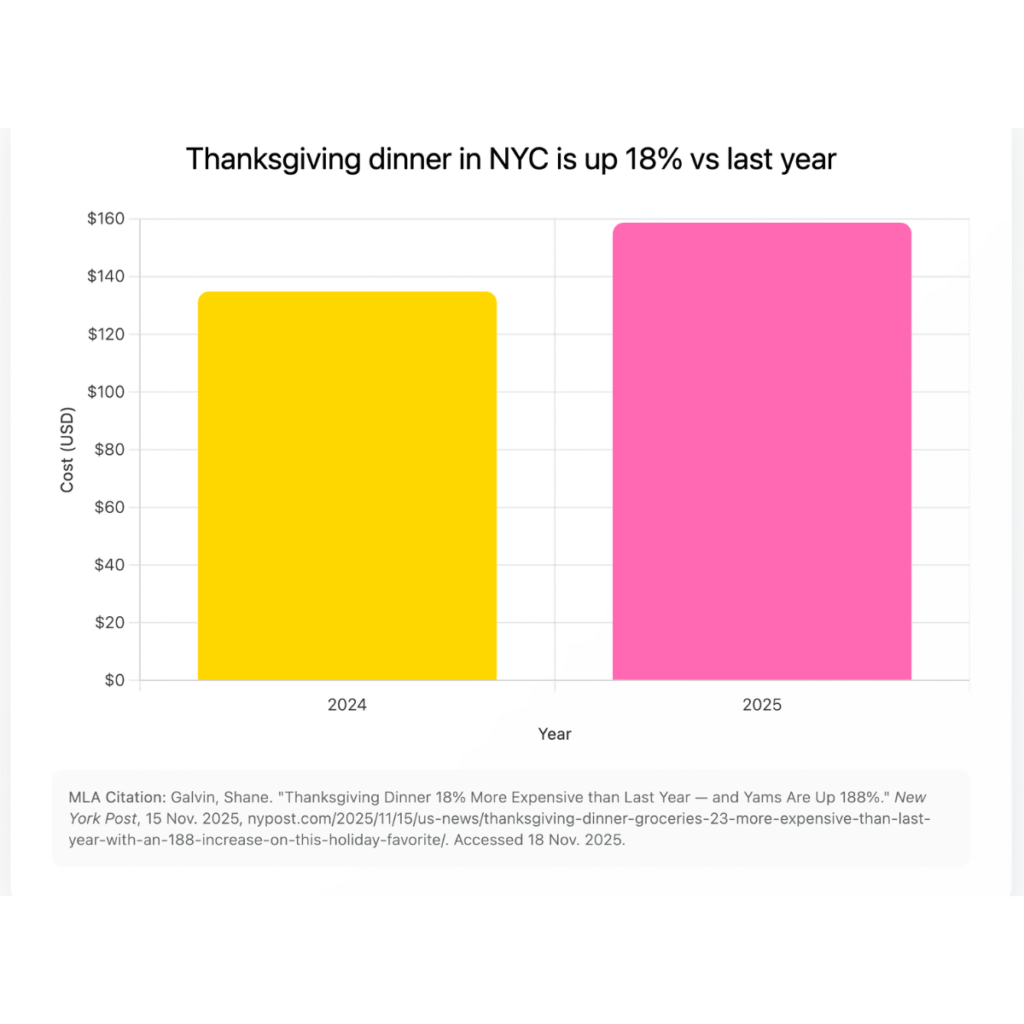

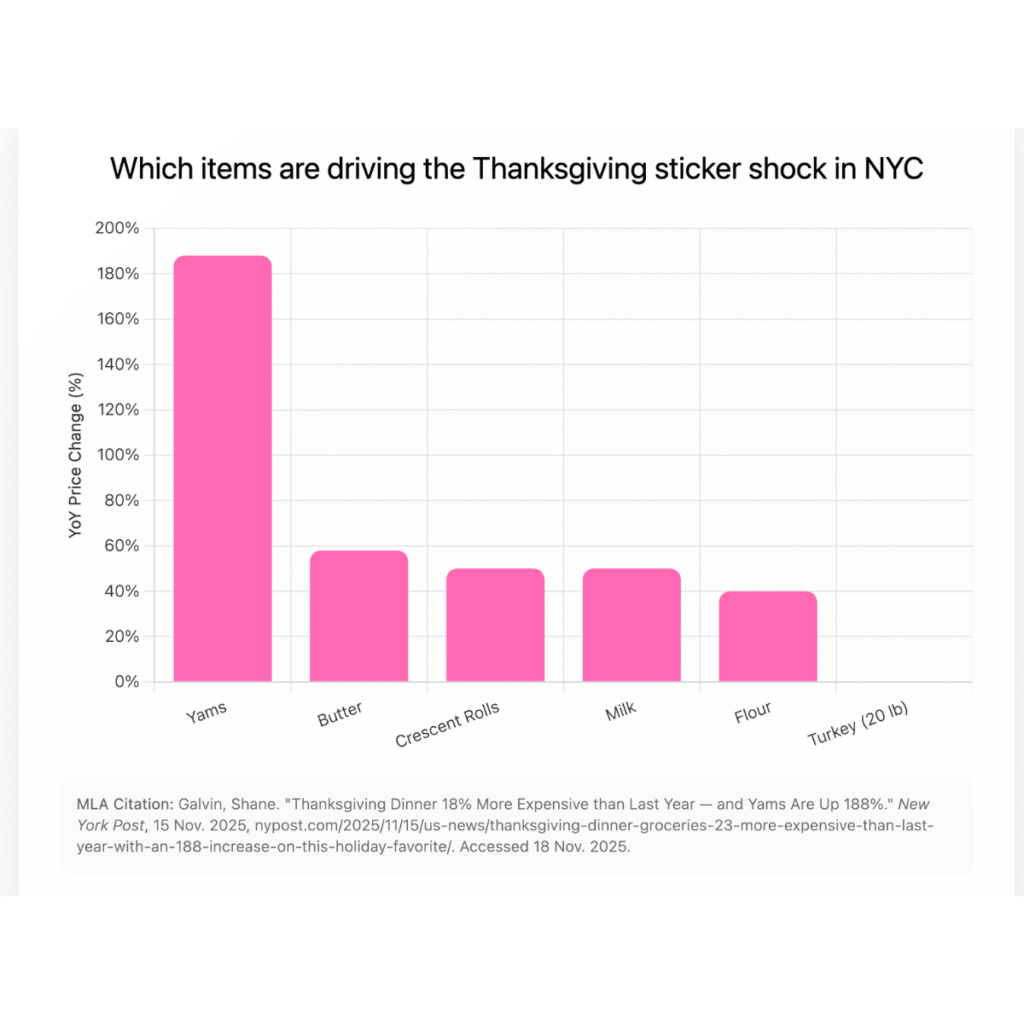

Look at Thanksgiving. One national analysis from a major bank says the average Thanksgiving basket is 2-3% cheaper than last year for a typical family meal. Other data from New York finds a dinner for ten up 18% versus 2024 with yams up 188%, butter up 60%, crescent rolls up about 50%, plus flour and milk up around 40-50%. Turkey itself is roughly flat in price but New Yorkers still pay more per pound than the national average.

So both stories are true. It depends where you live, which retailer you shop, how you define the “basket” and which year you choose as your comparison. That is November reality, not September.

On top of that, the tariff picture on food just flipped. Early this year, new import tariffs raised costs on coffee, bananas, beef and orange juice. Last week, the administration reversed that and exempted +200 food products, including many of those staples, after months of public frustration about grocery prices. Some exporters, like Brazil, still face very high tariffs on key products, so the relief is partial.

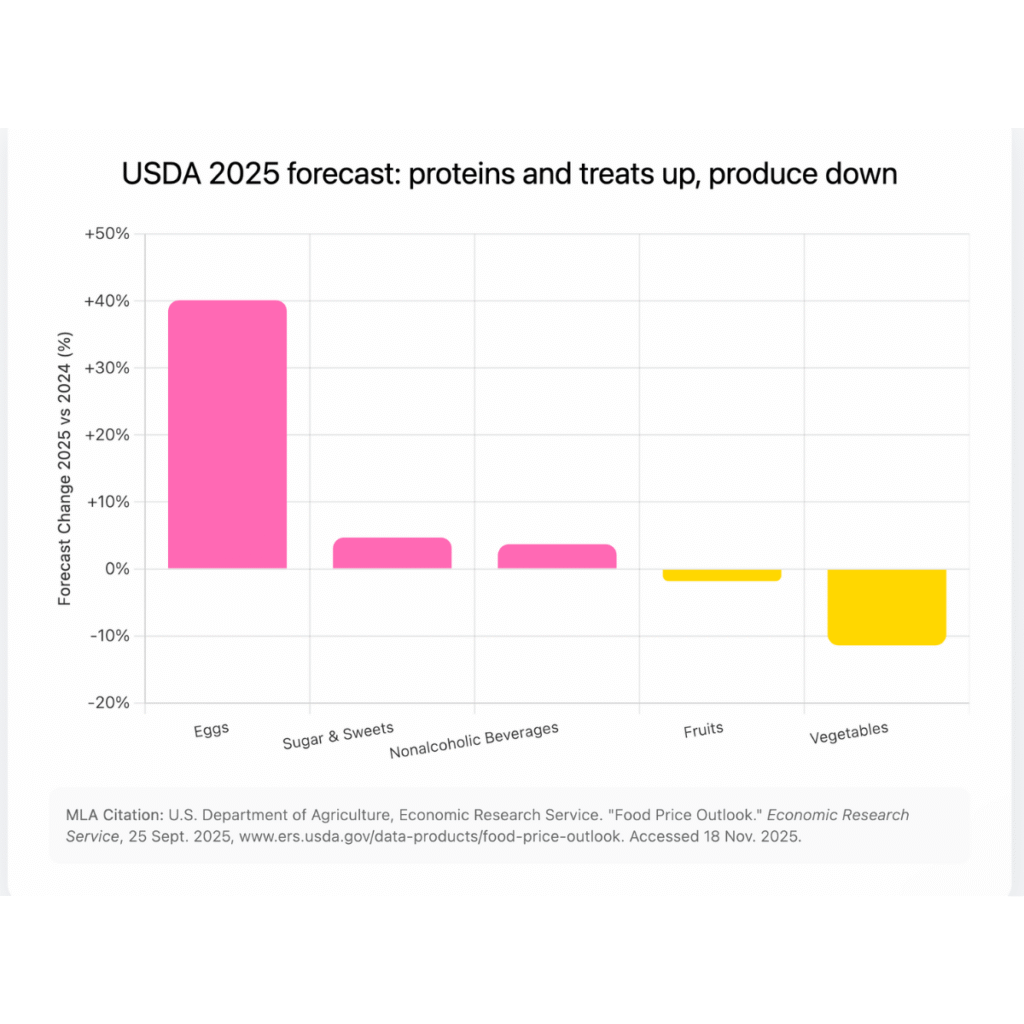

USDA data shows farm level cattle prices in August were about 26% higher than a year earlier and wholesale beef about 21% higher. Farm level fruits and vegetables were cheaper than a year ago and are projected to fall further in 2025. So proteins and treats up, produce down.

While inflation data is getting difficult, social listening data can fill gaps and monitor the frequency and sentiment of price mentions in product reviews and social media data, then compare that month over month or even week over week. For insight on how to setup a social listening system for monitoring inflation and consumer sentiment, feel free to reach me directly with any questions.