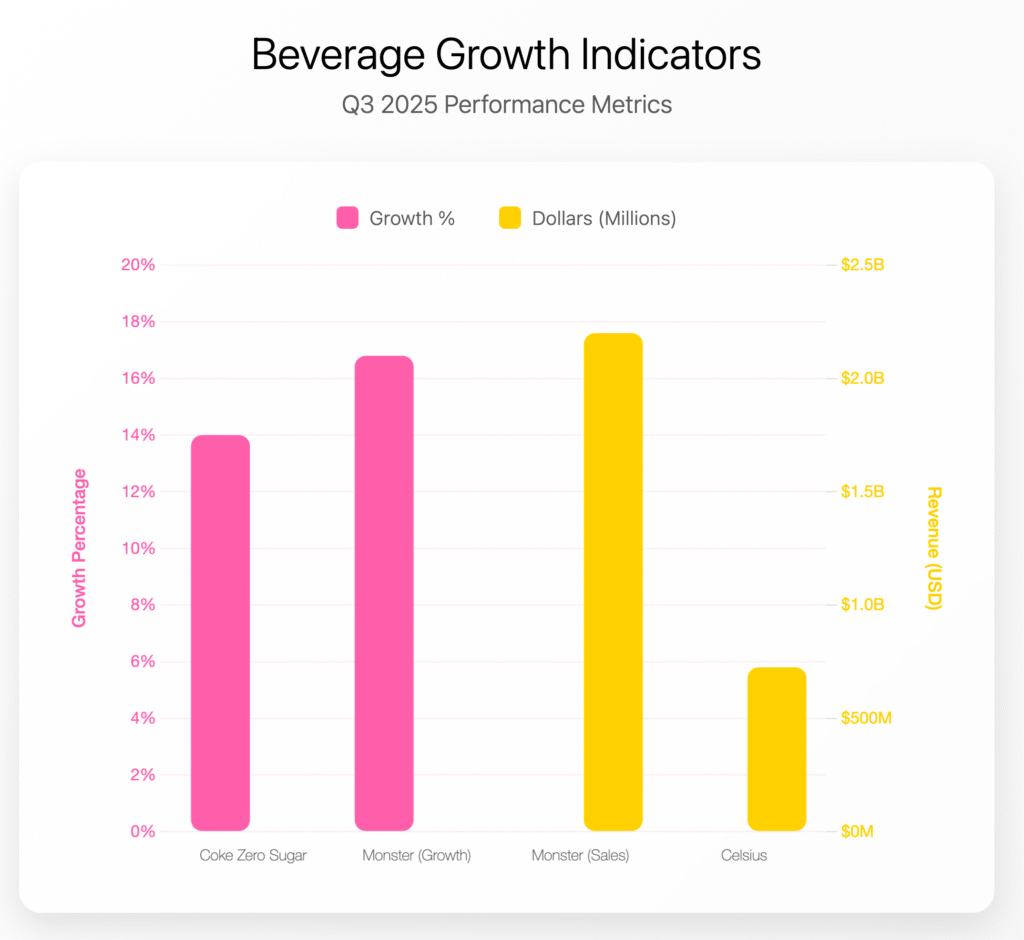

Zero sugar soft drinks are growing because taste finally meets the promise and because small packs fit tight budgets. Energy drinks are growing because they deliver a clear function with flavor variety and easy access in the cold vault. The latest quarter makes both points. Coca-Cola reports Coke Zero Sugar +14% in Q3 with broad gains across regions.

Energy is still compounding from a larger base. Monster printed +16.8% net sales growth to $2.2B in Q3 with stronger margins and continued strength in Ultra sugar-free lines and new flavors. Celsius reported $725M in Q3 revenue with continued distribution gains and international growth. Both companies benefit from the same pattern. Clear benefit before work or workouts. A calorie profile that fits a wellness mindset. Flavor churn that keeps the shelf fresh without confusing the purpose of the drink. Availability in the places people already stop.

In convenience and mass, the cold vault now treats energy drinks like a default or go to choice, not a niche or uncommon purchase. In grocery and eGrocery, small packs and minis make it easy to add a few cans to the basket without breaking the budget. Retail media then places the right pack at the right moment. A mini can in a deli cooler at lunch, a 12-pack on a pantry-stocking page, or an energy drink before a long drive. When content and price ladders move quickly, these categories do not need heavy ad bursts to maintain momentum. The shelf and the app do more of the work, which is where many brands are focusing their spend.